House Hacking 101 | Vol. 12

“If you have decent credit, a stable job, and a small amount of savings, you can enter the world of homeownership. And if you’re smart about it, you can enter the world of real estate investing at the same time and start hacking your living expenses.”

– Brandon Turner

The idea of “hacking” originated at MIT around pranks and mischief that usually required some technical expertise. It later became synonymous with criminal internet break-ins. Lately, it’s been rehabilitated into something Twenty Percenters love: finding novel workarounds to life’s challenges.

Today, we’ll explore house hacking as a way to make homeownership more affordable.

“House hacking” was coined on the BiggerPockets podcast by Brandon Turner in 2014. When investor Mark Ainley described how he rented out bedrooms to cover rent in college, Turner exclaimed, “You were hacking. I call that house hacking—where you buy a house, live for free because your buddies pay for it.”

House hacking is hardly a new idea. As far back as the 1800s, people ran boarding houses. They rented extra rooms to provide supplemental income. Today, when home prices conspire with mortgage rates to make homeownership feel out of reach, house hacking is a particularly useful strategy for first-time home buyers.

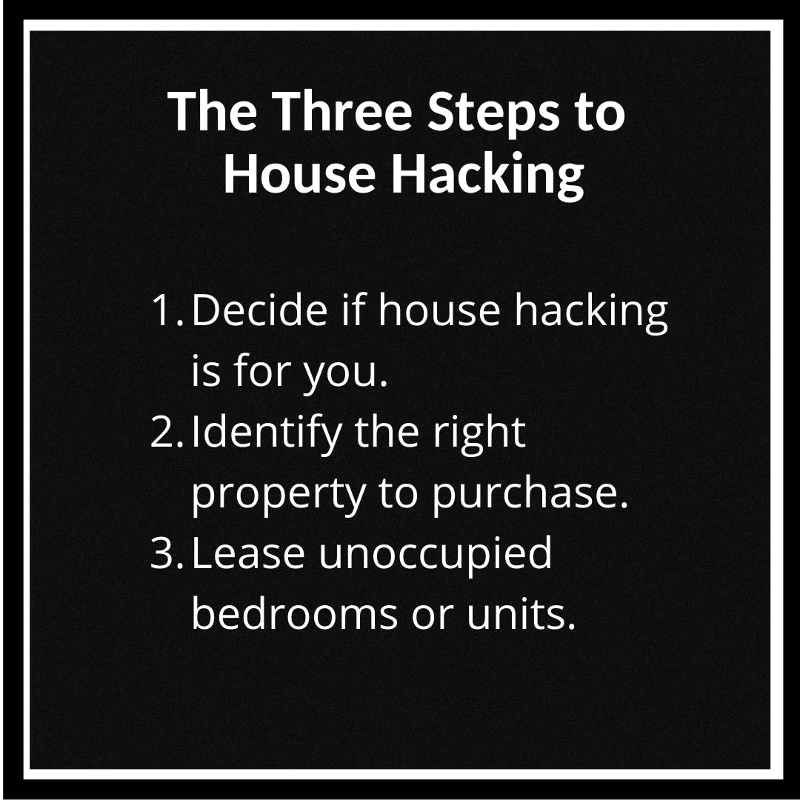

As real estate professionals, we know homeownership isn’t the right choice for everyone. The buyer has to both be financially capable to afford it and responsible enough to maintain it. While house hacking can solve the affordability issue, buyers should understand that house hacking comes with extra responsibilities. It’s not just about changing the AC filter and mowing the grass. House hacking combines homeownership with real estate investing. House hackers must screen tenants, understand leases, manage deposits, and collect rents. Depending on the property, they will also have to act as landlords and possibly even live with roommates.

For the right buyer, the benefits far outweigh the additional responsibilities. With leases in hand, a lender will likely consider the rental income as qualifying income. The lease income can pay for some or all of the owner’s mortgage expenses. They can also enjoy the normal benefits of ownership, like building equity and mortgage interest tax deductions.

After writing The Millionaire Real Estate Investor, our lead researcher Heather Iarruso bought her first home. She decided to live in the master suite and lease the other three bedrooms to grad students. The rental income covered virtually 100 percent of her mortgage. Later, when having roommates chaffed her lifestyle, she bought a condo for herself and kept the property as a full rental. The cash flow from her original property covered a lot of her condo mortgage as well. And voila, she transformed from a homeowner into an investor!

Once you’ve decided to try your hand at house hacking, deciding on the right property is a function of finances and lifestyle. While single first-time buyers may be more willing to have roommates in a single-family home, this is less attractive for buyers with a spouse or kids. In this situation, they can consider small, multifamily properties. Most duplexes, triplexes, and fourplexes qualify for conventional financing. A couple or a family would probably consider these the best options. They can also hunt for homes with rentable garage apartments, built-out basements, or ADUs (accessory dwelling units). These properties tend to be more common in more densely populated areas.

The final step in house hacking is to lease any unoccupied units or bedrooms. In my experience, house hackers can often fill initial vacancies by reaching out to their friends or personal network. While this saves on marketing costs, it can invite a hazardous level of informality. Leasing to friends is great from a roommate standpoint, but it can create real challenges when the rent is past due. Establish clear criteria for applicants. Set up a separate account for security deposits. Use promulgated forms for leases and enforce rental agreements evenly. Basically, treat the property like a business, because the IRS certainly will.

We cover the basics of house hacking in the newly released Your First Home, 2nd Ed. Still, if you or your buyers don’t know the basics of managing rentals in your market, that should be a prerequisite to pursuing this strategy.

Wendy and I bought our first home before we really understood the opportunities of house hacking. While we still own that first home and second homes as rentals, I have regrets. If I had a time machine, one of the first things I’d do is go back to 2001 and tell my younger self about house hacking. We probably would have started our homeownership journey with a duplex. And then bought a second duplex when we moved up. We’d have then had four streams of income (two duplexes + 4 units) to fund our first family home. Oh well. We did alright anyway, but let a boy dream.

One question to ponder in your thinking time: How can I incorporate house hacking into my first-time homebuyer and investor workshops?

Make an impact!

Jay Papasan

Co-author of The One Thing & The Millionaire Real Estate Agent

Leave a Reply

You must be logged in to post a comment.